CONTA SATÉLITE DA ECONOMIA SOCIAL (CSES) – COMO SE CONSTRÓI A CONTA SATÉLITE

Cristina Ramos Diretora de Serviço das Contas Satélite e Avaliação de Qualidade das Contas Nacionais do INE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . “Em 2016, o Valor Acrescentado Bruto (VAB) da Economia Social representou 3,0% do VAB da economia, tendo aumentado 14,6%, em termos nominais, face a 2013. Este crescimento foi superior ao observado no conjunto da economia (8,3%), no mesmo período.

A Economia Social representou 5,3% das remunerações e do emprego total e 6,1% do emprego remunerado da economia nacional. Face a 2013, as remunerações e o emprego total da Economia Social aumentaram, respetivamente, 8,8% e 8,5%, evidenciando maior dinamismo que o total da economia (7,3% e 5,8%, respetivamente). Por grupos de entidades da Economia Social, as Associações com fins altruísticos evidenciavam-se em número de entidades (92,9%), VAB (60,1%), Remunerações (61,9%) e Emprego remunerado (64,6%).” O INE publicou, em julho último, a terceira edição da Conta Satélite da Economia Social (CSES), para 2016. Este artigo surge como um complemento, tendo como objetivo explicar, em termos gerais, como se constrói esta conta satélite, no intuito de dar a conhecer aos utilizadores os “bastidores” deste projeto, ilustrando a complexidade e potencial deste produto estatístico. 1. As contas satélite e as Contas Nacionais A produção de Contas Nacionais consiste, em termos simplistas, em integrar, reconciliar e equilibrar diferentes fontes oficiais de informação, que já passaram por processos rigorosos de validação e análise de qualidade. Contudo, apesar da riqueza e qualidade da informação, as Contas Nacionais nem sempre permitem responder às necessidades de informação de utilizadores cada vez mais exigentes. Muitas vezes a informação de Contas Nacionais precisa ser reorganizada ou expandida, para melhor responder a necessidades de informação muito específicas. As contas satélite vieram, de certo modo, responder a esta exigência crescente, constituindo extensões com maior detalhe das Contas Nacionais, tendo como objetivo ampliar a capacidade de observação de fenómenos particulares. As contas satélite poderão ser consideradas um produto de elevado valor acrescentado, já que, utilizando fontes de informação e know-how residente nos institutos de estatística, permitem criar novos produtos estatísticos e melhorar a qualidade das Contas Nacionais (ao pesquisar novas fontes, detetar erros, testar metodologias alternativas). O facto dos resultados das contas satélite serem comparáveis com sistemas estatísticos estabelecidos torna este produto estatístico ainda mais apelativo. Com efeito, as Contas Nacionais tornaram-se, nos últimos anos, uma espécie de “língua franca” quando se fala de economia. É inegável o impacto da comunicação da relevância de determinado fenómeno quando se afirma que representa X% do Produto Interno Bruto (PIB) ou do Valor Acrescentado Bruto (VAB) da economia. Este é o tipo de quantificação que as contas satélite permitem, contrariamente a outros estudos, por seguirem métodos e fontes idênticos às Contas Nacionais. As contas satélite vieram também demostrar a grande utilidade das Contas Nacionais para utilizadores não habituais desta informação. Inúmeros manuais têm, por isso, vindo a ser desenvolvidos por organizações internacionais, para diferentes contas satélite, de modo a que os resultados sejam internacionalmente comparáveis. 2. A Conta Satélite da Economia Social (CSES) A Conta Satélite da Economia Social (CSES) surgiu na sequência de um desafio, lançado pela Cooperativa António Sérgio para a Economia Social (CASES) ao Instituto Nacional de Estatística (INE), no sentido de obter informação detalhada sobre a Economia Social, comparável com as Contas Nacionais portuguesas, quantificando, com rigor, a sua relevância na economia nacional. A CSES encontra-se, assim, integrada no quadro conceptual do Sistema de Contas Nacionais Portuguesas e tem como principal objetivo disponibilizar informação económica sobre a Economia Social. A escolha das Contas Nacionais como referência reflete a sua importância enquanto representação do funcionamento da economia, fiável, sistematizada e comparável internacionalmente. 2.1. A Base metodológica Todas as contas satélite portuguesas têm como primeiro referencial os conceitos e métodos das Contas Nacionais, definidos no Sistema Europeu de Contas Nacionais e Regionais. A CSES tem, desde o exercício de 2013, também como referência metodológica a Lei de Bases da Economia Social (Lei n.º 30/2013, de 8 de maio) que, entre outras matérias, estabelece o tipo de entidades que devem integrar a Economia Social, assim como os princípios orientadores que devem orientar as atividades desenvolvidas por estas entidades. Segundo a Lei de Bases da Economia Social, entende-se por Economia Social o conjunto das atividades económico-sociais, livremente levadas a cabo pelas Cooperativas, Associações Mutualistas, Misericórdias, Fundações, Instituições Particulares de Solidariedade Social (IPSS), Associações com Fins Altruísticos, que atuem no âmbito cultural, recreativo, do desporto e do desenvolvimento local, entidades abrangidas pelos Subsetores Comunitário e Autogestionário, integrados nos termos da Constituição no setor cooperativo e social, assim como por outras entidades dotadas de personalidade jurídica que respeitem os princípios orientadores da Economia Social. Na elaboração da CSES são igualmente considerados os conceitos, métodos, classificações e regras contabilísticas de manuais internacionais específicos. Estes manuais, além de constituírem referências, potenciam a comparação da CSES com outras experiências internacionais, embora, por vezes, seja necessário compatibilizar os diferentes entendimentos e métodos consagrados nos vários documentos. A CSES portuguesa constitui um projeto inédito em termos internacionais, pela sua abrangência e versatilidade. Quando a CSES foi inicialmente concebida não existia um referencial internacional único, pelo que foi necessário coordenar e adaptar os manuais existentes ("Manual for drawing up the satellite accounts of companies in the social economy: co‑operatives and mutual societies” do Centre International de Recherches et d'Information sur l'Economie Publique, Sociale et Coopérative - CIRIEC e Handbook on Non-Profit Institutions in the System of National Accounts” - Nações Unidas). As nomenclaturas ou classificações existentes eram, por um lado, mais relacionadas com a vertente não mercantil da Economia Social, ou idênticas às das Contas Nacionais (possuindo, por isso, menor detalhe e valor acrescentado). Neste contexto, o INE, em articulação com a CASES, procedeu à construção de uma nova nomenclatura, que melhor ilustrasse a realidade da Economia Social: a “Classificação de Atividades das Entidades da Economia Social (CAEES)”, que era uma adaptação da “International Classification of Nonprofit Organizations (ICNPO)”. Em 2018 as Nações Unidas disponibilizaram um novo manual: “Satellite Account on Non‑profit and Related Institutions and Volunteer Work”, com maior abrangência que o antecessor (compreendendo já as Cooperativas e Associações Mutualistas). Este manual resulta de vários anos de discussões com peritos internacionais e institutos de estatística (entre os quais o INE). Acompanhando os desenvolvimentos internacionais, o INE, com o acordo da CASES, decidiu, na CSES de 2016 (divulgada em 2019) passar a utilizar este manual como referencial metodológico. Não constituiu uma decisão fácil, uma vez que obrigou a um trabalho acrescido de reclassificação de unidades de atividade económica e condicionou a comparabilidade de dados com mais detalhe face a exercícios anteriores. Contudo, consideramos que se tratou de uma decisão necessária, num momento em que vários países na UE se preparam para começar a elaborar as suas contas satélite à luz deste novo manual. A comparabilidade internacional constitui um fator fundamental para a relevância de qualquer produto estatístico. 2.2. A compilação da CSES 2.2.1. O Universo As contas satélite (bem como as Contas Nacionais) têm como um dos seus objetivos principais, a exaustividade. Por isso, no caso específico da CSES, em cada exercício procede-se a uma inventariação exaustiva das unidades institucionais elegíveis no âmbito da definição de Economia Social. Este processo é habitualmente designado por “definição do universo”, que mais não é do que a definição do “perímetro” de análise, a identificação das unidades de atividade económica que serão acompanhadas e estudadas pela conta satélite. Além da identificação, nesta fase de trabalho as entidades são também classificadas de acordo com as tipologias pretendidas para o apuramento de resultados. Neste trabalho de identificação e classificação é necessário estabelecer contactos com várias entidades, embora o INE e a CASES detenham, indiscutivelmente, as principais fontes de informação relativas às diferentes entidades / organizações consideradas: o INE, enquanto instituto agregador da informação quantitativa, disponível de forma organizada e a CASES, como fonte de informação privilegiada sobre o setor cooperativo e, também, na relação que estabelece com outras entidades relevantes da Economia Social, no sentido de validar alguma da informação analisada. O universo da CSES (bem como das Contas Nacionais) não inclui as unidades de atividade económica que, na base de dados do INE, se encontram extintas ou inativas. A construção do universo da CSES parte do universo das Contas Nacionais, estabelecendo uma primeira classificação das unidades de acordo com a Lei de Bases da Economia Social:

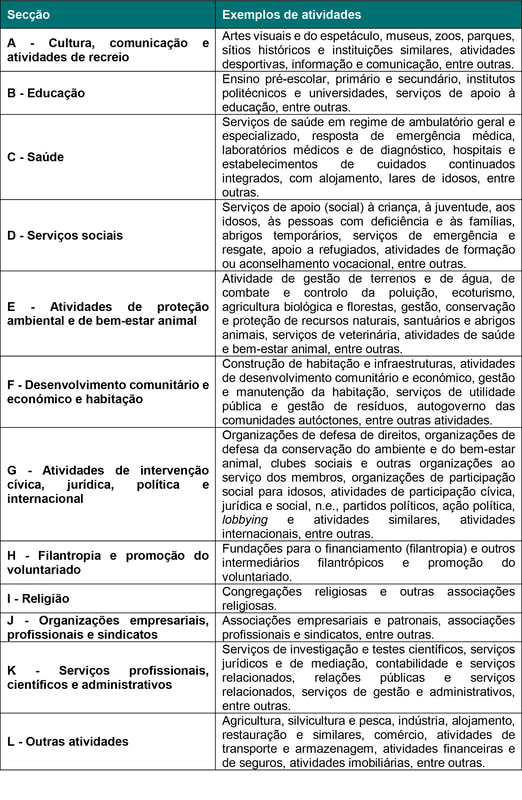

Importa ainda referir que são incluídas nos grupos das Misericórdias e das Associações Mutualistas as respetivas caixas económicas anexas, uma vez que o seu regime jurídico (Decreto-Lei n.º 190/2015, de 10 de setembro) estabelece que estas devem respeitar, com as devidas adaptações, os princípios orientadores que regem a atividade da Economia Social, bem como os princípios mutualistas previstos no Código das Associações Mutualistas, podendo apenas ser constituídas para a exclusiva prossecução dos fins de Associações Mutualistas, Misericórdias ou outras instituições de beneficência, observando‑se igualmente algumas restrições na afetação de resultados. Note-se que esta classificação das organizações da Economia Social não se encontra prevista em nenhum manual de contas satélite, apesar da maioria dos grupos considerados estarem representados no Comité Económico e Social Europeu pela Conferência Europeia Permanente – Cooperativas, Mutualidades, Associações e Fundações (CEP-CMAF). As Misericórdias, sendo entidades específicas de Portugal, originaram um grupo específico pela sua importância em termos sociais no nosso país. A divisão adotada corresponde, grosso modo, aos agrupamentos que congregam as entidades da Economia Social segundo a Lei de Bases da Economia Social, e segue a forma jurídica das organizações, de acordo com a tabela do Ficheiro de Unidades Estatísticas (FUE) do INE. São ainda classificadas as entidades detentoras do estatuto de IPSS ou equiparadas, uma vez que estas podem assumir diferentes formas e naturezas jurídicas, encontrando-se dispersas por todos os grupos de entidades da Economia Social. Na edição de 2016 da CSES foi criada uma classificação adicional das entidades detentoras de alguns estatutos especiais: as organizações não-governamentais de ambiente (ONGA), as organizações não-governamentais para o desenvolvimento (ONGD), as organizações não-governamentais das pessoas com deficiência (ONGPD), as associações não-governamentais de mulheres (ONGM) e as associações representativas dos imigrantes e seus descendentes (ARID). Adicionalmente, as unidades são classificadas de acordo com o setor institucional (nomenclatura de Contas Nacionais): sociedades financeiras, sociedades não financeiras, administrações públicas, famílias (vulgo empresários em nome individual) e instituições sem fim lucrativo ao serviço das famílias (onde se encontra a maioria das unidades de atividade económica da Economia Social). Nas administrações públicas estão classificadas as régie‑cooperativas (uma especificidade nacional). Por fim, as unidades que constituem o universo da CSES são também objeto de classificação em termos de atividade, de acordo com a “Classificação Internacional de Organizações Sem Fins Lucrativos e do Terceiro Setor”. O quadro seguinte descreve, genericamente, exemplos de atividades incluídas em cada uma das seções desta classificação:

Quadro 1

Classificação Internacional de Organizações Sem Fins Lucrativos e do Terceiro Setor (CIOSFL/TS) – Exemplos de atividades Sempre que possível, a informação referente à secção L – Outras atividades é apresentada desagregada, dada a relevância da mesma, nomeadamente nas Cooperativas e nas Associação Mutualistas (atividades financeiras e de seguros, mais concretamente).

Destacam-se como principais alterações com impacto na CSES 2016, as seguintes:

O critério de classificação é a atividade principal da unidade institucional. É importante referir que a construção do universo é uma fase do trabalho particularmente morosa, minuciosa e complexa, sendo, no entanto, crucial para a qualidade final do produto estatístico. Este é um trabalho habitualmente “invisível” para o utilizador. A morosidade e complexidade anteriormente referidas encontram-se geralmente relacionadas com alguns problemas recorrentes, relacionados com dificuldades na identificação nominal e fiscal das entidades ou incoerências quanto à sua situação perante a atividade ou atividade desenvolvida. Contudo, no decurso das diferentes edições da CSES tem sido sempre possível ultrapassar os problemas registados, através de análises conjuntas efetuadas entre o INE e a CASES, contactos com as entidades, recolha de dados administrativos, etc. É importante referir que este processo beneficiaria fortemente da criação da base de dados das entidades da Economia social, prevista na Lei de Bases da Economia Social, com elevados ganhos de eficácia e agilização da elaboração da CSES. Esperamos que numa futura edição da CSES o INE possa contar já com esta informação. 2.2.2. Tratamento e análise da informação Após a delimitação do universo, são compiladas variáveis económicas, integradas numa sequência de contas, adiante descrita. Nos parágrafos seguintes encontram-se descritas cada uma dessas contas, de modo sumário. A Conta de Produção compreende as operações associadas ao processo produtivo das entidades envolvidas. Apresenta a Produção como recurso e o Consumo intermédio como utilização. A diferença entra as duas operações corresponde ao Valor Acrescentado Bruto – VAB, que constitui o saldo da conta. A produção inclui:

A Economia Social é constituída por unidades institucionais muito diversas, a operar nos setores não mercantil e mercantil da economia nacional, embora a maioria apresente essencialmente produção não mercantil. A produção para utilização final própria é praticamente residual na Economia Social. A Conta de Exploração analisa em que medida o VAB permite cobrir as Remunerações e os Outros impostos à produção líquidos de Outros subsídios à produção. Mede o Excedente de Exploração Bruto, que constitui o excedente (ou o défice) resultante das atividades produtivas, antes de serem tidos em consideração os juros, as rendas ou encargos que a unidade produtiva deve pagar pelos ativos financeiros ou pelos recursos naturais que obteve por empréstimo ou locação e que deve receber pelos ativos financeiros ou pelos recursos naturais de que é proprietária. Contrariamente à Conta de Exploração, a Conta de Afetação dos Rendimentos Primários diz respeito às unidades e setores institucionais residentes, enquanto beneficiários, e não como produtores, de Rendimentos primários. Consideram-se “Rendimentos primários” os rendimentos de que dispõem as unidades residentes em resultado da sua participação direta no processo produtivo e os rendimentos que recebe o proprietário de um ativo financeiro ou de um ativo corpóreo não produzido em retribuição da colocação destes à disposição de uma outra unidade institucional. A Conta de Distribuição Secundária do Rendimento evidencia a forma como o saldo dos rendimentos primários de um setor institucional é afetado pela redistribuição: impostos correntes sobre o rendimento, o património, etc., contribuições e prestações sociais (com exceção das transferências sociais em espécie) e outras transferências correntes. O saldo da conta é o Rendimento disponível, para Consumo final ou Poupança. No âmbito desta conta, as Contribuições sociais são registadas como utilizações do setor institucional das Famílias e como recursos dos setores institucionais responsáveis pela gestão da segurança social. Quando se trata de Contribuições sociais que os empregadores devam pagar em benefício dos seus trabalhadores, essas contribuições devem ser primeiro incluídas nas Remunerações dos empregados, no lado das utilizações da Conta de Exploração dos empregadores, dado que integram os custos salariais; são igualmente registadas, como Remunerações dos empregados, no lado dos recursos da conta de Afetação dos Rendimentos Primários das Famílias, visto corresponderem às prestações atribuídas às Famílias. A Conta de Redistribuição do Rendimento em Espécie dá uma imagem mais ampla do rendimento das Famílias, ao integrar os fluxos correspondentes à utilização de bens e serviços individuais de que estas Famílias beneficiam a título gratuito das Administrações públicas e das Instituições sem fim lucrativo ao serviço das famílias, isto é, Transferências sociais em espécie. As Transferências sociais em espécie são registadas no lado dos recursos da conta de Redistribuição do Rendimento em Espécie, no caso das Famílias, e no lado das utilizações, no caso das Administrações públicas e das Instituições sem fim lucrativo ao serviço das famílias. O saldo da conta da Redistribuição do Rendimento em Espécie é o Rendimento disponível ajustado. A Conta de Utilização do Rendimento Disponível inclui a noção de despesa de Consumo final financiada pelos diversos Setores envolvidos: Famílias, Administrações públicas e Instituições sem fim lucrativo ao serviço das famílias. O saldo da Conta de Utilização do Rendimento Disponível constitui a Poupança. A Conta de Utilização do Rendimento Disponível Ajustado inclui a noção de Consumo final efetivo, que corresponde ao valor dos bens e serviços de que dispõem efetivamente as Famílias para Consumo final, mesmo que a sua aquisição seja financiada pelas Administrações públicas ou pelas Instituições sem fim lucrativo ao serviço das famílias. Em consequência, o Consumo final efetivo das Administrações públicas e das instituições sem fim lucrativo ao serviço das famílias corresponde ao Consumo final coletivo. A nível do total da economia, despesa de Consumo final e Consumo final efetivo são noções equivalentes; só são diferentes as repartições entre os setores institucionais. O mesmo se passa com o Rendimento disponível e o Rendimento disponível ajustado. A Poupança é o saldo contabilístico das duas versões da conta de Utilização do Rendimento. O seu valor é idêntico para todos os Setores, independentemente de ser obtido deduzindo ao Rendimento disponível a despesa de Consumo final ou deduzindo ao Rendimento disponível ajustado o Consumo final efetivo. A Poupança é o montante (positivo ou negativo) resultante das operações correntes que estabelece a ligação com a acumulação. Se a Poupança é positiva, o rendimento não despendido é destinado à aquisição de ativos ou à redução de passivos. Se a Poupança é negativa, certos ativos são liquidados ou certos passivos aumentam. Por fim, a Conta de Capital permite determinar em que medida as Aquisições líquidas das cessões de ativos não financeiros foram financiadas pela Poupança e pelas Transferências de capital. Revela uma capacidade de financiamento correspondente ao montante de que uma unidade ou um setor dispõem para financiar, direta ou indiretamente, outras unidades ou setores, ou uma necessidade de financiamento, que corresponde ao montante que uma unidade ou setor tem de pedir emprestado a outras unidades ou setores.

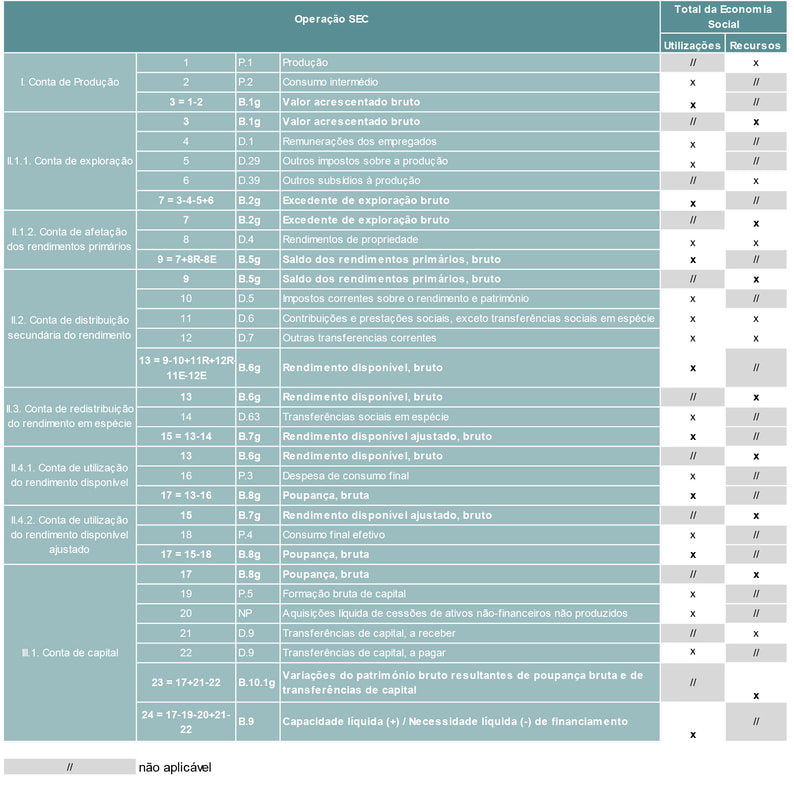

Quadro 2

Sequência completa de Contas para a análise da Economia Social Na CSES portuguesa a sequência completa de contas (até à capacidade/necessidade de financiamento) é elaborada para a Economia Social total, bem como para os grupos de entidades cuja informação é mais completa: Cooperativas e Associações Mutualistas. Com efeito, as Cooperativas e Associações Mutualistas têm apresentado uma cobertura quase exaustiva em termos de fontes de informação contabilística, registando-se maiores dificuldades na obtenção de informação para os restantes grupos da Economia Social, em particular para as Fundações, as ACFA e os SCA. Estas dificuldades ao nível da disponibilidade de informação de base e da respetiva consistência não garantem o rigor necessário ao cálculo do conjunto de variáveis da sequência completa de contas até ao saldo da Capacidade / Necessidade líquida de financiamento, para todos os grupos de entidades. A estimativa de emprego da CSES consiste, numa primeira etapa, em determinar o número de empregos associados a cada entidade no universo de referência. A fonte de informação para os postos de trabalho é, sempre que possível, a mesma fonte de dados utilizada para o cálculo das remunerações dos empregados e produção, de modo a que a informação geral sobre cada unidade seja a mais consistente possível. Uma vez concluídos os trabalhos, os postos são convertidos em equivalente a tempo completo (ETC) que é definido como o total de horas trabalhadas dividido pelo número médio anual de horas trabalhadas em empregos a tempo inteiro no território económico, que é obtido aplicando conversores das Contas Nacionais. 2.2.3. Principais fontes de informação A CSES é compilada a partir de fontes de informação já existentes, não existindo inquéritos adicionais criados propositadamente para este projeto (reside aqui um dos pontos fortes das contas satélite em geral e da CSES em particular). As principais fontes de informação para o apuramento das variáveis monetárias e não monetárias são: INE

Outras fontes

A abordagem de compilação da conta satélite baseia-se numa relação estreita com o Sistema de Contas Nacionais. Para qualquer setor institucional, sempre que possível, recorre-se às mesmas fontes de informação, aplicam-se os mesmos métodos e compararam-se os resultados finais. 3. Considerações finais Em conclusão deste artigo, que encerra o ciclo de trabalho na elaboração e divulgação da terceira edição da CSES, apresentam-se as seguintes reflexões:

Disclaimer: As opiniões expressas neste artigo são da exclusiva responsabilidade da autora, não vinculando o INE. |

ENG

SOCIAL ECONOMY SATELLITE ACCOUNT (CSES) – HOW THE SATELLITE ACCOUNT IS BUILT

Cristina Ramos Head of Service of Satellite Accounts and Quality Assessment of National Accounts at INE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . “In 2016 the Gross Value Added (GVA) of Social Economy represented 3.0% of the GVA of the economy, a 14.6% increase, in nominal terms, when compared with 2013. This growth was higher than that recorded in the economy as a whole (8.3%) in the same period.

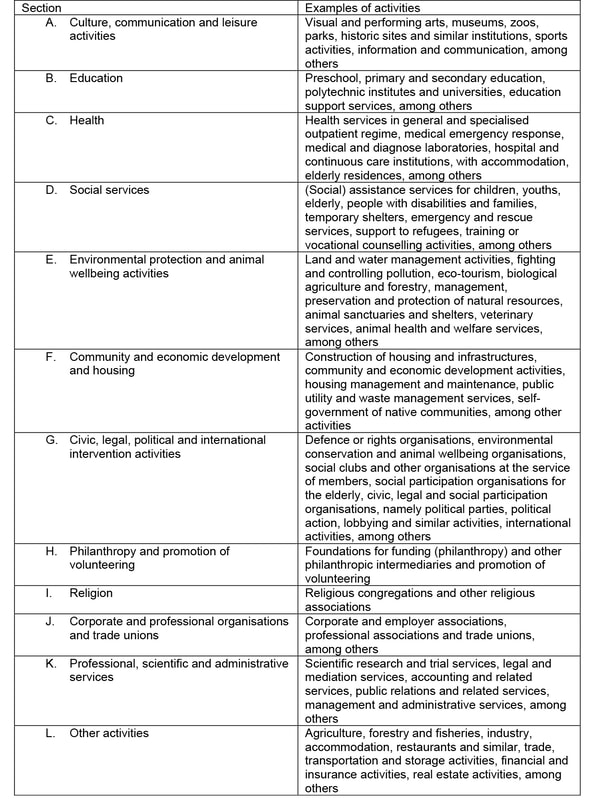

Social Economy represented 5.3% of wages and total employment and 6.1% of paid employment in the national economy. Compared with 2013, the remuneration and total employment of Social Economy increased, respectively, 8.8% and 8.5%, showing greater dynamism than the economy as a whole (7.3% and 5.8%, respectively). By groups of Social Economy entities, Associations with altruistic purposes stood out in number of entities (92.9%), GVA (60.1%), Remuneration (61.9%) and Paid employment (64.6%). “Last July, INE published the third edition of Social Economy Satellite Account (CSES) for 2016. This paper is a complement, aiming to explain, in general terms, how this satellite account is built, in order to make users aware of the “behind the scenes” of this project, illustrating the complexity and potential of this statistical product. 1. Satellite Accounts and National Accounts The production of National Accounts consists, in simplistic terms, of integrating, reconciling and balancing different official sources of information that have undergone rigorous processes of validation and quality analysis. However, despite the wealth and quality of information, National Accounts do not always allow meeting the information needs of increasingly demanding users. National Account information often needs to be reorganised or expanded to better respond to very specific information needs. Satellite accounts have, in a way, responded to this growing demand, constituting extensions of National Accounts in greater detail, with the aim of expanding the ability to observe particular phenomena. Satellite accounts can be seen as a product with high added value, since, using sources of information and know-how residing in statistical institutes, they allow creating new statistical products and improving the quality of National Accounts (by seeking new sources, detecting errors, testing alternative methodologies). The fact that the results of satellite accounts are comparable with established statistical systems makes this statistical product even more appealing. Indeed, National Accounts have, in recent years, become a sort of “lingua franca” when it comes to economics. The impact of communicating the relevance of a given phenomenon is undeniable when one claims that it represents X% of the Gross Domestic Product (GDP) or Gross Value Added (GVA) of the economy. This is the type of quantification that satellite accounts allow, contrary to other studies, for following methods and sources identical to National Accounts. Satellite accounts have also shown the great utility of National Accounts for non-usual users of this information. Therefore, numerous handbooks have been developed by international organisations for different satellite accounts, so that the results are internationally comparable. 2. Social Economy Satellite Account (CSES) Social Economy Satellite Account (CSES) came about following a challenge, launched by the António Sérgio Cooperative for Social Economy (CASES) to the National Statistics Institute (INE), in order to obtain detailed information on Social Economy, comparable with Portuguese National Accounts, accurately quantifying their relevance in the national economy. CSES is thus integrated into the conceptual framework of the Portuguese National Accounts System and its main aim is to provide economic information on Social Economy. The choice of National Accounts as a reference reflects their importance as a representation of the functioning of the economy, reliable, systematised and internationally comparable. 2.1. The methodological basis All Portuguese satellite accounts are based on the concepts and methods of National Accounts, as defined in the European System of National and Regional Accounts. Since 2013, CSES has also used the Basic Social Economy Act as a methodological reference (Law no. 30/2013, of May 8th) which, among other matters, establishes the type of entities that must integrate Social Economy, as well as the guiding principles that should guide the activities developed by said entities. According to the Basic Social Economy Act, Social Economy is understood as the set of economic and social activities, freely carried out by Cooperatives, Mutual Associations, Misericórdias, Foundations, Private Social Solidarity Institutions (IPSS), Associations with Altruistic Purposes, operating in the cultural, leisure, sport and local development fields, entities covered by the Community and Self-managed Subsectors, integrated under the terms of the Constitution in the cooperative and social sector, as well as other entities with legal personality that respect the guiding principles of Social Economy. In the preparation of CSES, the concepts, methods, classifications and accounting rules of specific international handbooks are also considered. These handbooks, in addition to being references, enhance the comparison of CSES with other international experiences, although, at times, there is a need to reconcile the different understandings and methods enshrined in the different documents. The Portuguese CSES is an unprecedented project in international terms, due to its scope and versatility. When CSES was initially conceived, there was no single international reference, so it was necessary to coordinate and adapt the existing handbooks (“Handbook for preparing the satellite accounts of Social Economy companies: cooperatives and mutual societies” of the Centre International de Recherches et d’Information sur l’Economie Publique, Sociale et Coopérative - CIRIEC and “Handbook on Non-Profit Institutions in the System of National Accounts” - United Nations). The existing nomenclatures or classifications were, on the one hand, more related to the non-market aspect of Social Economy, or identical to those of National Accounts (therefore having less detail and added value). In this context, INE, in conjunction with CASES, built a new nomenclature, which better illustrated the reality of Social Economy: the “Classification of Activities of Social Economy Entities (CAEES)”, which was an adaptation of the “International Classification of Non-profit Organisations (ICNPO)”. In 2018, the United Nations released a new handbook: “Satellite Account on Non profit and Related Institutions and Volunteer Work”, with greater coverage than the predecessor (now including Cooperatives and Mutual Associations). This handbook is the result of several years of discussions with international experts and statistical institutes (including INE). Following international developments, INE, with the agreement of CASES, decided, in the 2016 CSES (released in 2019), to use this handbook as methodological reference. It was not an easy decision, since it required an increased work of reclassification of units of economic activity and conditioned the comparability of data in more detail compared with previous years. However, we believe that this was a necessary decision, at a time when several countries in the EU are preparing to start drafting their satellite accounts in the light of this new handbook. International comparability is a critical factor for the relevance of any statistical product. 2.2. The compilation of CSES 2.2.1. The universe One of the main objectives of satellite accounts (as well as National Accounts) is exhaustiveness. For this reason, in the specific case of CSES, each year, an exhaustive inventory of eligible institutional units is carried out under the definition of Social Economy. This process is usually called “definition of the universe”, and is no more than the definition of the “perimeter” of analysis, the identification of the units of economic activity that will be monitored and studied by the satellite account. In addition to identification, in this work phase entities are also classified according to the types intended for calculation of results. In this identification and classification work, one has to establish contacts with several entities, although INE and CASES undoubtedly have the main sources of information related to the different entities/organisations considered: INE, as an institute aggregating quantitative information, available organised, and CASES, as a source of privileged information about the cooperative sector and also in the relationship it establishes with other relevant entities of Social Economy, in order to validate some of the information analysed. The CSES universe (as well as National Accounts) does not include units of economic activity that are extinct or inactive in the INE database. The construction of the CSES universe is part of the National Accounts universe, establishing early classification of units according to the Basic Social Economy Act: • Cooperatives; • Mutual Associations; • Misericórdias; • Foundations; • Community and Self-managed Subsectors (SCA); • Associations with Altruistic Purposes (ACFA). It should also be noted that the respective attached savings banks are included in the Misericórdias and Mutual Associations groups, since their legal regime (Decree-Law no. 190/2015, of September 10th) establishes that they must respect, with due adaptations, the guiding principles that govern the activity of Social Economy, as well as the mutual principles provided for in the Code of Mutual Associations, which can only be constituted for the exclusive pursuit of the purposes of Mutual Associations, Misericórdias or other charitable institutions, also observing restrictions on the allocation of results. Note that this classification of Social Economy organisations is not set forth in any handbook of satellite accounts, although most of the groups considered are represented on the European Economic and Social Committee by the Permanent European Conference – Cooperatives, Mutual Entities, Associations and Foundations (CEP-CMAF). Misericórdias, entities specific to Portugal, originated a specific group due to their social importance in our country. The division adopted corresponds, roughly, to the groupings that bring together Social Economy entities according to the Basic Social Economy Act, and follows the legal form of organisations, according to the table of the Statistics Unit File (FUE) of INE. Entities with IPSS status or similar are also classified, since they can take on different forms and legal natures, dispersed among all groups of Social Economy entities. The 2016 edition of CSES introduced an additional classification of entities holding special statuses: non-governmental environmental organisations (ONGA), non-governmental development organisations (ONGD), non-governmental organisations for people with disabilities (ONGPD), non-governmental organisations for women (ONGM) and associations representing immigrants and their descendants (ARID). Additionally, the units are classified according to the institutional sector (nomenclature of National Accounts): financial corporations, non-financial corporations, public administration, families (aka individual entrepreneurs) and non-profit institutions serving families (including most economic activity units in Social Economy). Public administrations include regie-cooperaties (a national specificity). Finally, the units in the CSES universe are also subject to classification in terms of activity, according to the “International Classification of Non-profit and Third Sector Organisations”. The following table describes, generically, examples of activities included in each of the sections of this classification:

Table 1

International Classification of Non-profit and Third Sector Organisations (CIOSFL/TS) – Examples of activities Where possible, the information related to section L – Other activities is shown disaggregated, given its relevance, namely in Cooperatives and Mutual Associations (financial and insurance activities, more specifically).

The main changes with an impact on CSES 2016 stand out, as follows: • Transfer of social clubs (examples: numismatics, philately, maximaphily, car fan clubs, movie clubs, etc.) from the scope of culture, communication and leisure activities to civic, legal, political and international intervention activities; • Transfer of scientific research from the scope of education to professional, scientific and administrative services; • Transfer of activities classified with code 87 of ISIC Rev. 4 (corresponding to division 87 of NACE Rev.2 and section 87 of CAE Rev.3) from the scope of social services for health. The classification criterion is the main activity of the institutional unit. It is important to mention that the construction of the universe is a particularly slow, detailed and complex work phase, albeit crucial for the final quality of the statistical product. This is a job that is usually “invisible” to the user. The aforementioned slowness and complexity are generally related to recurring problems, concerning difficulties in the nominal and fiscal identification of entities or inconsistencies regarding their situation in relation to the activity developed. However, during the different editions of CSES it has always been possible to overcome the problems recorded, through joint analyses carried out between INE and CASES, contacts with the entities, collection of administrative data, etc. It is important to note that this process would benefit greatly from the creation of the database of social economy entities, set forth in the Basic Social Economy Act, with high gains in efficiency and streamlining the preparation of CSES. We hope that in a future edition of CSES, INE will already have this information. 2.2.2. Information processing and analysis After the delimitation of the universe, economic variables are compiled, integrated into a sequence of accounts, described below. The following paragraphs describe each of these accounts, in short. The Production Account comprises operations associated with the production process of the entities involved. It presents Production as a resource and intermediate consumption as use. The difference between the two operations corresponds to the Gross Value Added – GVA, which constitutes the account balance. Production includes: • Mercantile production; • Production for own final use – goods and services retained for final consumption or capital formation by the same unit; • Other non-mercantile output – output supplied to other entities free of charge or sold at economically insignificant prices. Social Economy is made up of very different institutional units, operating in the non-mercantile and mercantile sectors of national economy, although most of them essentially record non-mercantile production. Production for own final use is practically residual in Social Economy. The Operating Account analyses the extent to which the GVA allows covering Remunerations and Other taxes on production, net of Other production subsidies. It measures Gross Operating Surplus, which constitutes the surplus (or deficit) resulting from productive activities, before taking into account interest, rent or charges that the productive unit must pay for the financial assets or natural resources it obtained on loan or lease and that which it must receive for financial assets or natural resources that it owns. Unlike the Operating Account, the Primary Income Allocation Account relates to resident institutional units and sectors, as beneficiaries, not as producers, of primary income. “Primary income” means income available to resident units as a result of their direct participation in the production process and income received by the owner of a financial asset or tangible non-produced asset in return for making it available to another institutional unit. The Secondary Income Distribution Account shows how the balance of primary income in an institutional sector is affected by redistribution: current taxes on income, wealth, etc., contributions and social benefits (with the exception of social transfers in kind) and other current transfers. The account balance is Disposable Income, for Final Consumption or Savings. Under this account, Social Contributions are recorded as uses of the institutional sector of Families and as resources of the institutional sectors responsible for the management of social security. When it comes to Social Contributions that employers must pay to the benefit of their workers, these contributions must first be included in Employee Compensation, on the side of the employers’ Operating Account, as they are part of salary costs; they are also recorded as Employee Compensation, on the resource side of the Primary Income Allocation Account of Families, since they correspond to benefits attributed to Families. The Income Redistribution in Kind Account provides a broader picture of Families’ income, by integrating the flows corresponding to the use of individual goods and services that these Families benefit from free of charge from Public Administrations and non-profit institutions serving families, that is, social transfers in kind. Social transfers in kind are recorded on the resource side of the Income Redistribution in Kind Account, in the case of Families, and on the uses side, in the case of public administrations and non-profit institutions serving families. The balance of the Redistribution of Income in Kind account is adjusted disposable income. The Disposable Income Use Account includes the notion of final consumption expenditure financed by the different Sectors involved: Families, Public Administrations and non-profit institutions serving families. The balance of the Disposable Income Use Account constitutes Savings. The Adjusted Disposable Income Use Account includes the notion of final effective Consumption, which corresponds to the value of the goods and services that families actually have for final consumption, even if their acquisition is financed by public administrations or non-profit institutions at the service of families. As a result, the effective final consumption of public administrations and non-profit institutions serving families corresponds to the collective final consumption. At the level of the total economy, Final Consumption and Actual Final Consumption expenses are equivalent notions; only the breakdowns between institutional sectors are different. The same applies to disposable income and adjusted disposable income. Savings is the accounting balance of the two versions of the Income Use account. Its value is identical for all Sectors, regardless of whether it is obtained by deducting the Final Consumption expense from Disposable Income or by deducting the effective Final Consumption from Adjusted Disposable Income. Savings is the amount (positive or negative) resulting from current operations that establishes the link with accumulation. If Savings is positive, unspent income is used to acquire assets or reduce liabilities. If Savings is negative, certain assets are liquidated or certain liabilities are increased. Lastly, the Capital Account allows determining the extent to which Acquisitions net of assignment of non-financial assets were financed by Savings and Capital Transfers. It reveals a financing capacity corresponding to the amount that a unit or sector has to finance, directly or indirectly, other units or sectors, or a financing need, which corresponds to the amount that a unit or sector has to borrow from other units or sectors.

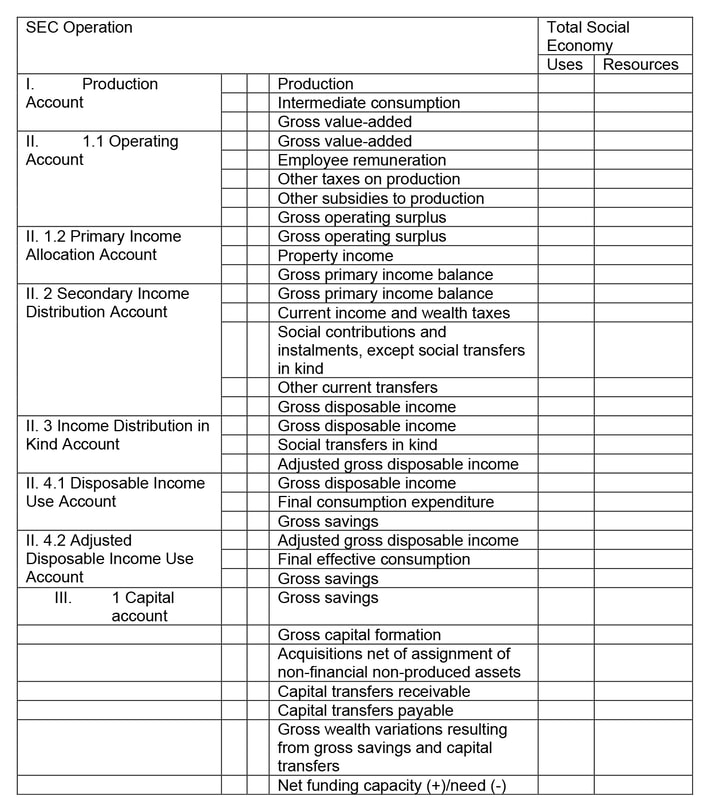

Table 2

Complete sequence of accounts for the analysis of Social Economy In the Portuguese CSES the full sequence of accounts (up to the funding capacity/need) is prepared for total Social Economy, as well as for the groups of entities whose information is more complete: Cooperatives and Mutual Associations. In effect, Cooperatives and Mutual Associations have presented almost exhaustive coverage in terms of sources of accounting information, with greater challenges in obtaining information for other groups of Social Economy, in particular Foundations, ACFA and SCA. These challenges in terms of availability of basic information and its consistency do not guarantee the necessary rigor in calculating the set of variables in the full sequence of accounts up to the balance of Net Funding Capacity/Need, for all groups of entities. The employment estimate of CSES consists, firstly, in determining the number of jobs associated with each entity in the reference universe. The source of information for jobs is, where possible, the same source of data used to calculate the remuneration of employees and production, so that the general information on each unit is as consistent as possible. Once work is completed, jobs are converted into full-time equivalent (ETC), defined as the total hours worked divided by the average annual number of hours worked in full-time jobs in the economic territory, obtained by applying converters from National Accounts. 2.2.3. Main sources of information CSES is compiled from existing sources of information, with no additional surveys created specifically for this project (here lies one of the strengths of satellite accounts in general and CSES in particular). The main sources of information for calculating monetary and non-monetary variables are: INE • National Accounts – the use of several work files stands out, including estimates for operations of the European Accounts System (Production, Intermediate Consumption, Remuneration, GVA, subsidies and taxes, among others); • General Statistical Units File (FUE) – the statistical units file is an instrument for coordinating and harmonising information relating to companies, establishments, groups of companies and vehicles. Companies are classified in different types, such as companies, single proprietors, non-profit institutions and public administration. FUE receives information from the different statistical operations of INE under the responsibility of the organic units of collection and statistical production and also includes administrative records from external entities; The integrated file system is supported by a computer application, which allows online management and updates for all FUE units and variables; • Survey of Employers’ Associations, Unions, Federations and Confederations (IAP) - specific survey applied to a particular fraction of the group of associations and other entities of Social Economy, which gathers information related to physical indicators (number of organisations, persons employed, etc.) and income and expense accounts of the Accounting Standardisation System (SNC), by type of employer organisation; • Survey on Mutual Aid Associations (IASM) – statistical operation that allows obtaining disaggregated information on financial and physical indicators related to the activity of Mutual Aid Associations; • Employment Survey (IE) – quarterly sample survey that provides quarterly and annual results. It aims to allow characterising the labour market in Portugal, namely the behaviour of employment and unemployment. It is from this survey that official statistics of the condition regarding work and other characteristics of the Portuguese population related to the labour market are produced, such as the sector of economic activity and profession, education and vocational training, demand for employment and professional path; • Survey of Fire Department Owners (IEDCB) – its main aim is to obtain physical and financial data related to fire prevention and fire fighting activities. In this survey, fire brigades in articulation with proprietor entities that own and maintain them active are surveyed, namely Mainland professional, mixed (only for fire brigades dependent on a city council) and private fire brigades and entities holding professional, mixed, voluntary and private fire brigades in the Autonomous Regions of the Azores and Madeira. With regard to financial data, the information relates to expenditure, income and investments relating to fire departments; • Survey on Environmental Non-Governmental Organisations (IONGA) - this statistical operation is part of the current production of Environment Statistics and aims to obtain physical data (nature of members, activities developed and personnel employed) and financial data (investments, expenses and income), according to the SNC for this group of entities. Other sources • Detailed analytical balance sheets of central administration entities; • Archeevo database of the General Secretariat of the Ministry of Internal Affairs; • General State Account (CGE); • Monthly statement of remunerations to Social Security - summarises the values of Remunerations, average number of persons employed in the year and number of working days per entity registered with Social Security. This database is provided to INE by the Social Security Informatics Institute, IP; • Income statement and balance sheets of Cooperatives credited by CASES. • Simplified Business Information (HEI) – mandatory tool for all organisations, including, among others, four important Attachments with different applications: • Annex A: applied to resident entities primarily engaged in commercial, industrial or agricultural activity and non-resident entities with permanent establishment; • Annex B: companies in the financial sector; • Annex C: companies in the insurance sector; • Annex D: resident entities that do not carry out, principally, commercial, industrial or agricultural activity. • Survey on the National Scientific and Technological Potential (IPCTN) –the official instrument (part of the National Statistical System) for accounting human resources and expenditure on research and development (R&D), following criteria agreed at European level by Eurostat and in conjunction with the OECD; • Listings of the Directorate-General for Social Security; • IPSS Budget and Accounts (OCIP) – represents a set of accounting obligations that IPSS and equivalent are required to fulfil, from the moment they register as IPSS in Social Security; • Reports and Accounts; • Single Report from the Strategy and Planning Office of the Ministry of Labour, Solidarity and Social Security; • Webpages of economic activity units; • Ministry of Justice website The approach to compiling the satellite account is based on a close relationship with the National Account System. For any institutional sector, where possible, the same sources of information are used, the same methods are applied and the final results are compared. 3. Final remarks To conclude this paper, which closes the work cycle in the preparation and dissemination of the third edition of CSES, the following reflections are offered: • With the presentation of results of CSES 2016, the National Statistical System and its users now have sector, robust, updated and consistent information with National Accounts, about the main variables that characterise Social Economy nationwide; the information is available on the INE portal (highlight, tables and info-graphics), in fully bilingual versions; • Albeit in the third edition, CSES should still be considered a project under development, due to the emergence of new realities, with consequent updating and permanent renewal of the concepts and methodologies adopted for the compilation of information, always in line with the evolution recommended by international reference institutions, such as the UN, Eurostat and CIRIEC; • The work to prepare CSES is sometimes more complex than expected, revealing not only the requirement for methodological rigor, but, above all, fragility and, more often than desired, lack of credible and up-to-date sources of information for the sector. The availability and quality of basic information is critical to the quality of any statistical product. It is crucial to raise awareness, on the part of Social Economy entities, of the relevance of information for the acknowledgment and development of their activity and their role as providers of information; • Despite its importance as a “portrait” of the economic dimension of Social Economy, CSES is only a partial view thereof. In fact, the analysis of the relevance of Social Economy should not be limited to the economic component, but include information of a broader spectrum, such as members/associates, beneficiaries, externalities, multiplier effects and impacts, information that transcends the scope of CSES. It was in this sense that INE launched, in May 2019, a survey that characterises the exhaustive sector (“Survey on Social Economy Sector”), raising questions about the activities developed, internal composition, relations established with public and private sector entities, labour relationship model, role of volunteering in the direction and development of the activity, qualification and remuneration of workers, collaborators and managers of these entities, among others. The results of this innovative statistical operation will be announced later this year and will certainly be an extremely important milestone in knowledge about the sector. Disclaimer: The opinions expressed in this article are the sole responsibility of the author and do not bind INE. |